On 30 June 2019, we completed 5 years of our darling – CityFALCON. Over the last 5 years, I’ve followed my passion (not “worked”) – a lot. On average about 60 hours a week, 50 weeks a year. That gave me 15,000 hours of experience as an entrepreneur, and that isn’t even counting the work an entrepreneur does during “off times”. So below, I’m outlining the 15 most important things I’ve learned over my 15,000 hours of entrepreneurship.

That’s about 1,000 hours per lesson, so if it takes you 30 seconds to read a section, you’ll be gaining 1,000 hours of entrepreneurial wisdom in 30 seconds. Great deal, isn’t it?

In that time, my team and I have managed to raise £1.8 million in angel and crowdfunded investments, and we’ve grown the team to 37 people. We have recently expanded to Malta and will be over 50 employees soon.

If you want to start from the very beginning, I’ve documented the journey over the last five years on this section of our blog. The posts are intermittent, but they give a general overview. But if you just want the nuggets of wisdom, simply read on.

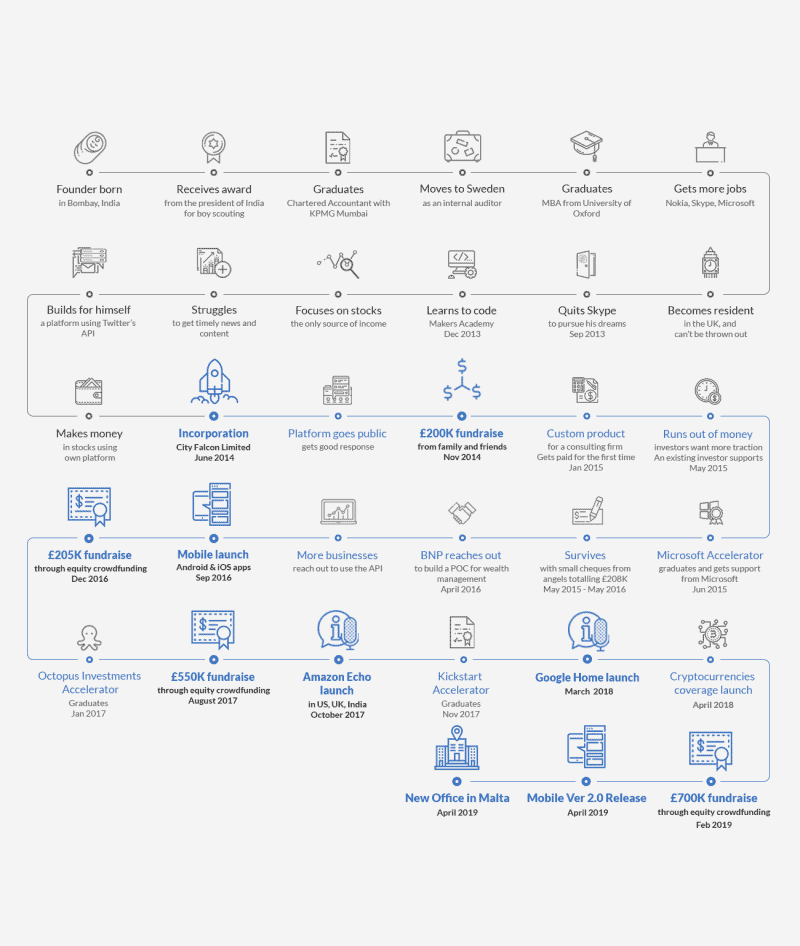

This is where our journey has taken us so far:

0. Run with your idea

Okay, so actually there are 16, but 15 lessons from 15,000 hours rolls off the tongue better than 16 lessons from 15,000 hours. So we’re going to call this Lesson 0 – and it really is kind of preliminary to starting any kind of entrepreneurial journey.

Most people will say that you need to have a solid idea of your product before you can even start, a thorough business plan, find co-founder(s), think everything through completely – but the reality is that if you do all those things, you will never start. Stop procrastinating, start doing – build landing pages, prototypes, whatever it is for you to go beyond just the idea stage. Yes, there is a 90% chance that you might fail but at least you tried – most people just don’t move beyond the I have an idea stage. A great analogy often used for this is that you need to jump off the cliff and build the parachute on your way down 😉

For tech entrepreneurs, you need to understand your product, and that includes understanding computer systems and how to code. Naturally not every tech startup founder is going to be a star programmer, but if you don’t understand the basics, it will be hard for you to communicate with your engineers. This leads to overpromising and underdelivering to clients and pissing off your engineers. So if you’re in the tech space, even if you have a brilliant plan for commercialisation, have a great network, and are charismatic, it still pays immensely to know at least a little code.

1. Life is not fair; just deal with it

My first entrepreneurial nugget of wisdom is pretty useful for life, too. Some companies will raise hundreds of millions of dollars while you’re left struggling to raise a few hundred thousand. Statistically, you’re likely to be the latter, and not many are going to care about you.

And when you’re only raising a couple hundred thousand dollars, you’ll also be struggling to win awards, garner media attention, and get your message out there. Your product might even be awesome, but, to be fair to the publicisers, there are tens or hundreds of products competing for eyeballs. They can’t cover them all.

Consider every failure of an accelerator application and every rejection letter from a media outlet as another instance of experience, and don’t let them kill your spirit. Remain calm and soldier on. Once you win that first award or snag that first major headline, it will become much easier. You’ve been recognised, which gives you a level of credibility with investors and other media outlets.

2. Stop listening to the startup media and the wrong people

I just said you’ll build credibility with the media. Well, don’t listen to them anyway. As you probably noticed, they’re mostly interested in publishing stories with established interest, which means many good people and good ideas are overlooked.

Moreover, no one publishes failures, unless it was a crash-and-burn scenario where thousands of people were laid off or the company collapsed in spectacular fashion. And failure is not all negative, as long as it doesn’t crush the foundation of the company and the team.

So don’t obsess over the media and the buzz. Do, however, listen to the right people. Those people could become your mentors. Look at industry contacts, management experience, commercialisation success, fundraising track record. Don’t overlap advisor knowledge too much until you have more money and time. One great, well-founded opinion is better than multiple mediocre, poorly defended opinions.

A word of caution if you are looking for advise on how to run your company, or raise funds, etc. – take advice from those entrepreneurs who have done these things. You will meet several people who claim to have worked or advised startups but not actually run a company or raised funds. Don’t blindly follow their advice. I’ve made that mistake a few times.

Lastly, the media portrays fundraising as simple. Many keyboard warriors believe it to be so, too. Just hop on to Kickstarter or Seedrs or GoFundMe and you’ll be rolling in the cash. Not true. Want to see how hard it is to raise money? Do a demo for someone interested in your product and idea, then try getting 500 quid out of them. If they’re an average, wage-earning worker, it’ll probably be harder than you think. Based on my experience of raising more than £1.8 million, there are only two things that will help you raise funds: FOMO and relationships. Read more here.

3. There is no one “right way” to build a business

You’ll get plenty of advice, much of it unsolicited. And much of it will be textbook strategy to starting a business. This might work for some people, but if this is your first business, it probably won’t go nearly as smoothly as those textbook strategies assume.

Back to Point 1: sometimes the billion-dollar idea is recognized for what it is, and sometimes it isn’t. Entrepreneurship is more of an art than a science and an element of luck and timing is woven throughout.

Other than laws, there aren’t any rules. Break social norms and you might go viral – positively or negatively. Break establishment rules and … be a disrupter. In the tech space, breaking the “rules” may actually be a better path to success than religiously copying established customs, companies, and people.

Remember that the Silicon Valley way of running business by raising hundreds of millions in funding is not the only way. There are companies that have become successful and in some cases unicorns by building companies in a more sustainable way than just burning cash. Besides, not everyone has tens of millions in cash to burn. You need to make what you have work for you.

4. Your idea will be fluid

You may think you have your plans all laid out, but things will change. The Agile methodology is very popular in the tech startup world for a reason: if you can’t adapt and do so quickly, you’ll perish. Your basic product idea will shift as you speak to investors and potential customers. The former are funding your project, and they’ll want to have some say. The latter are also funding your project, and they will voice their opinions with their wallets. At CityFALCON, we log every instance of feedback from users and investors, be it via email or social media. It’s a goldmine for ongoing UX research.

You will often see startups “pivoting” by changing the product, business model, or other important components. It’s common and necessary; don’t fight it..

One important corollary is to avoid “building in stealth”. Don’t ask a few people and embark on a grand product building campaign in secret. It is hard enough to align the visions of a few employees let alone capture the attention of faceless customers and agreement from tens of investors with widely varying backgrounds.

Get constant feedback and adapt accordingly. Maintain a fundamental thread that connects all your actions, but make sure the thread is elastic and not a solid steel fetter.

5. Avoid VC money unless otherwise impossible

You know who gets the media attention? Venture capitalists. Sure, you will get collateral coverage when a big-name VC funds your venture, but they’re probably funding multiple other companies as well. And for benefiting from their name recognition and connections, you’ll pay dearly.

VCs want fast ROI, and they may not care about your product, your team, or you. That sounds harsh, but their goal is generally to make money as fast as possible. That means building up and exiting. Their money often comes with overbearing terms like preference shares, veto rights, and double-dips. if they grab a large part of your equity, they’ll assuredly use it to their advantage and the potential disadvantage of founders, early investors, and employees. Apart from the horror stories in the media, I’ve heard of some really strange stories from fellow entrepreneurs.

Personally, I’ve pitched to several VCs, mostly in Europe. We didn’t get funding, but what worried me most was the questions they asked. It was clear that they had never run a business before. They were approaching my company from their own background: all finances and management consulting, no entrepreneurship. Don’t let consultants and bankers who have never built a company dictate to you how to run yours just because they throw dollars at you.

6. Get close to new and serial entrepreneurs

Networking is essential in running a business, and networking with other entrepreneurs is part of the game. Spending time with serial entrepreneurs will bring you into contact with plenty of wisdom. They’ll help you avoid paths that are likely to fail. They’ll also bring you into contact with potential investors, and they might even recommend you.

As you grow in your role as an entrepreneur, pay it forward. You never know when a newer entrepreneur will turn out to be a huge business opportunity, future partner, or simply someone full of great ideas. And you can take satisfaction that you’ve helped someone else realise their project.

7. Build a robust hiring process and strategy

When you start a company, it will be small by default. That means you need to find some of the best talent to bring your product to fruition, but you won’t have the financial firepower to pay a lot. Luckily, there are plenty of highly talented people attracted to the more dynamic world of startups than corporate life, so people are still interested.

That said, no matter what you think about hiring and which people will fit which roles, you will learn a lot about management during your journey. One way to screen applicants is technical tests, which we have done at CityFALCON for designers, developers, and financial analysts. But don’t forget about company fit. The most brilliant programmer won’t be able to keep your entire team afloat if everyone else hates him/her.

You need to strike a balance between great technical skills and interpersonal skills. Startups often require overtime, and your team has to like each other to spend that much time, for that little pay, with each other.

8. Financial perseverance – live to fight another day

We’ve been in a situation where our liquid assets (i.e. cash) – which is basically all our assets because we have no infrastructure – amounted to less than the payroll liabilities at the end of the month. Actually, we’ve been in that situation 5 times. And we’ve spend significant time in “the danger zone”, where cash is starting to run thin. Sometimes we operate in that zone for months, as shown here (blue stripe is the danger zone):

At those times you may question your abilities as a leader. The people who depend upon you for their livelihoods are in danger of not being paid, and your ship is sinking. If you’ve built a strong team (Lesson 7), your employees probably won’t abandon ship from a single late payment. But investors will ask why the hell you need another cash injection – didn’t you just have one 8 months ago?

Those can be dark times. Take some deep breaths, do some meditation or yoga or whatever you do to remain calm, and soldier on. You’ll make it through. And if you don’t, well, you aren’t in some tiny minority. Plenty of startups fail. It’s a rough personal experience, but it is an experience that will teach you much about entrepreneurship and your resolve in when failure is near at hand.

At the same time, you will be tempted with cushy jobs with good, guaranteed month-end salaries. It isn’t uncommon for entrepreneurs abandon their own ships for more financial security.

Do whatever it takes to survive. I’ve taken loans from existing investors and friends, issued more stock options in lieu of cash salaries, and personally forwent salary for a whole year.

9. Find your balance

Speaking of rough times, you’ll run into many. Conversely, there will be many highs: first big client, first major investor, first time your product hits the market, when you realise the growth of your user base is accelerating.

Taking the good with the bad, you’re apt to average out to neutral. However, humans aren’t computers. In the moment, it is hard to put the situation into perspective within the longer term. You need to find a few techniques to remain calm, during both highs and lows.

Some people meditate. Some do yoga. Some play sports. Some ride motorcycles. Some take long hikes in the mountains or long walks on the beach. Whatever it is, make sure to remain calm and balanced, and avoid destructive behaviours like drinking and smoking. Competitive sports can help take your mind off things by focusing on the competition, which can give you the balance you need (see Lesson 10).

Calm and balance will help you prevent making rash decisions when riding high and making desperate decisions when falling low.

The key here is mental balance.

10. Don’t ignore your body

Much of the process of business building takes place in the mind. But your mind lives within your body, so you can’t neglect your body. Working out and participating in sports serves multiple purposes. It can be a way to keep you calm and balanced. It can be a way to relieve stress. It also keeps your body in good condition, which transfers to a good mental state.

The saying a sound mind in a sound body isn’t baseless. It is very important to keep a sound body. If you’re sick, how well do you work? Besides, there is scientific evidence that exercise releases hormones that positively influence your brain, which is your mind’s house.

The key here is corporeal stability.

11. Get comfortable with the unknown

First, no one knows everything. There are going to be multiple scenarios in which you don’t know how to proceed or respond. This is when you lean on your network and let your employees use their own judgement.

Become comfortable with proceeding blindly. Have a plan, but allow for significant alternations to the plan. If you, nor your team, nor your advisors have clear paths to move forward, you’ll have to leap into the unknown.

In the startup world, you’ll probably be doing this often.

12. Your word is final

Now I’ve said in multiple lessons that it is important to take advice and learn from people. However, at the end of the day, it is still your company. You make the decisions. If someone’s advice directly conflicts with your goals or intuitions, you are not required to apply it.

It can be difficult to judge when advice that goes against your goals is well-founded. This is why balance and calmness are so important. You need to think logically through your decisions. If you have a strong feeling for Method A, but someone is recommending Method B, you have to look deeply into why B is better. Review the issues, determine your level of competence in the area, and weigh the pros and cons. There will always be this temptation to reach a middle ground between A and B, and at most times, it would be the wrong decision to make.

In the end, no one knows your business better than you do, so sometimes Method B might be wired for failure within your very specific setting. Introducing a compromised solution may seem successful at first, only to crash down later. Ultimately you have to take responsibility for the decision. Back yourself!

13. You need advice, but you need hands (and minds) more

Naturally people will give you advice. Are they always willing to help you accomplish that advIce? Not in the slightest. You’ll also have a lot of employees willing to work part-time. This stems partially from insecurity of work, as startups do fail or can’t pay people sometimes. They might want your company as a side gig with a more stable job elsewhere.

But you need people to do the work, and depending on your company, you will have a lot of work to do. If you don’t have full-time commitments, you may consistently be relegated to the “when I have time” column of priorities. People rarely have the time.

Get full-time commitments from employees. They need to prioritise your position over others. They can have side gigs, but you should be the main gig.

14. Don’t rely on others without question or blindly

It’s just business, as they say, but you may feel screwed over. I don’t want to say this is common in entrepreneurship, but you shouldn’t rely on anyone. I started the business as a sole founder. No service, no employee should be irreplaceable. Your head of marketing might be your flatmate, but money makes people do funny things. It may not be malicious, either. Sometimes the right opportunity presented itself and the person cannot pass it up.

Service providers are not bound by similar close human connections, so you should always have replacements in mind. Moreover, many service providers know they are dealing with a small company and may try to strongarm you into less favourable terms. Don’t simply accept it. Shop around and go to another provider if you can find a better deal.

Make sure no one is irreplaceable and keep good relations, so your employees, investors, or service providers will give you ample advanced notice before leaving.

Regarding performance evaluation, teach yourselves the basics of everything that you need to manage the business: coding, accounting, legal work, projections, and any other critical component. You don’t need to know everything, but you need to know the basics to ensure employees and service providers are delivering accurate information and products. I even do filings with SEC, Companies House, and other government agencies myself or thoroughly review the work done by service providers.

It’s your ship. You need to know how to steer it when something goes wrong or someone doesn’t deliver support or accuracy as expected.

15. Don’t fear failure

Many startups fail, either wholly or in part. A product might flop. Your technical implementation might not perform well. A client might drop out, decimating half your revenue. You will be forced to make decisions you are not wholly confident in. You will have conflict with investors and employees.

Any of these things can lead to failure. But don’t fear it. Fear leads to paralysis, and paralysis will definitely lead to failure.

If you do fail, figure out why and move on. You can even take some of your more supportive advisors and employees with you. If they can discern your leadership skills, some of them might stick around for another idea.

In Summary

So that’s my 15 lessons of entrepreneurship for you. Of course there are plenty of others, and you’ll certainly have your own set of 15 after your first 15,000 hours. It’s a journey, and you’ll always need to rethink and reshape yourself and your company.

Do you have any Lessons you find crucial but didn’t see on my list? Add them below in the comments. Maybe in Year 10 I will write a blog about the 30 Lessons I Learned from 30,000 Hours of Entrepreneurship.

Leave a Reply