На рынках царит хаос, приближающийся к полной панике как к роману. коронавирус, также известный как COVID-19, и его последствия вызывают недовольство рынков, нарушают цепочки поставок, а политики изо всех сил пытаются сдержать вирус и успокоить общественность. В S&P500 снизился на 10% за последний месяц; как FTSE и DAX снизились на 20% в Европе; и Японии Nikkei 225 упал 17%, в то время как корейский КОПСИ упала на 11%, а гонконгский Hang Seng 8%. Масло сильно пострадал и вызвал массовую распродажу акций, когда сам товар упал на 21% за один уикенд в ответ на обвал ОПЕК переговоры и новая ценовая война между Россия и Саудовская Аравия. Для инвесторов все становится только хуже, и многие видят в этом время для выхода с рынков.

Это не единственный спад, который мы наблюдали за последние два десятилетия, и, по крайней мере, до сих пор, лопнувший пузырь доткомов и финансовый кризис 2008 года, безусловно, сильно ударили по рынкам. В последнее десятилетие было несколько неприятностей, таких как крах в Китае в 2016 году, когда инвесторам больше не разрешалось выводить свои деньги. И для наших читателей, занимающихся криптоинвестированием, 2018 год был определенно жестоким. Но рынки капитала не боролись с глубоким спадом почти 12 лет, когда в 2007-2008 годах началась Великая рецессия.

Но сейчас время инвестировать? Мы думаем, что было бы разумно подождать немного и посмотреть, как обстоят дела на рынках, прежде чем прыгать, чтобы извлечь выгоду из паники последних нескольких дней и более медленного спада в прошлом месяце.

Все аргументы и мнения в этой статье не следует рассматривать как финансовые советы, и вполне возможно, что мы ошибаемся в этих прогнозах. Это «пища для размышлений», а не «вещественные доказательства для принятия инвестиционных решений». пожалуйста не использовать наш блог как единственный источник информации для принятия инвестиционных решений!

1 - Рынки переоценены, и запаса прочности нет

Сегодня, 10 марта 2020 года, рынки дешевле, чем на прошлой неделе или в прошлом месяце? Конечно. Но они не дешевле, чем были год назад. Они все еще переоценены сейчас, и будут таковыми до тех пор, пока не упадут ниже своих внутренних значений. Только в этом случае появится так называемый «запас прочности», когда рыночная цена ниже внутренней стоимости. И только тогда большинство ценных инвесторов сочтут их подходящими объектами инвестирования.

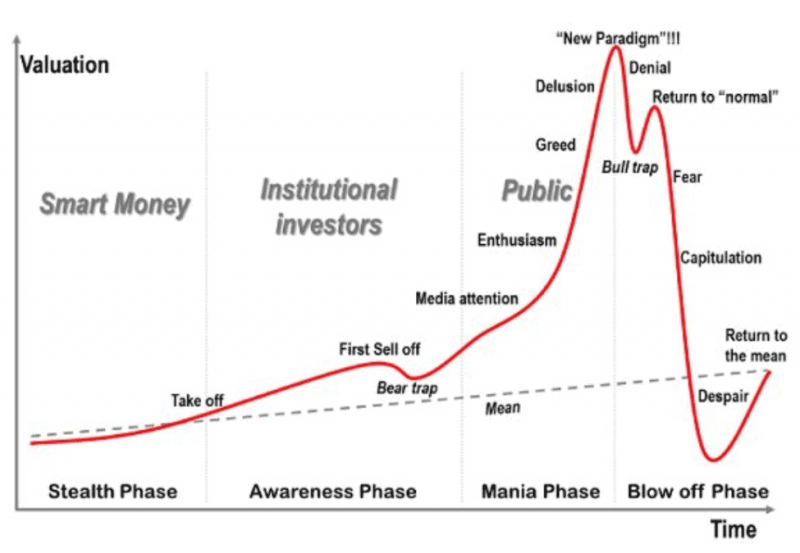

Также поучительно поразмышлять над этим графиком анатомии пузыря:

Источник: д-р Жан-Поль Родриг, факультет глобальных исследований и географии, Университет Хофстра.

Поскольку мы видели, как рынки растут, поднимаются и растут, кажется, что мы движемся к стадии «отрицания» и, вероятно, увидим отскок вскоре после паники, поразившей рынки сегодня. Этот отскок вызван инвесторами, которые считают, что общая ситуация не так уж плоха, рынки не переоценены и что предыдущий тренд продолжит восходящую траекторию.

То, находимся ли мы в пузыре, всегда подтверждается только после того, как крах миновал, но если вы считаете, что акции в настоящее время переоценены с исторически высокими коэффициентами PEG, то вы можете избегать покупок во время шторма в течение пары недель или месяцев, пока не наступит реальный кровавая бойня.

2 - Избыточное кредитное плечо и ликвидность исчезнут по мере поступления требований маржи

Уровни кредитного плеча и ликвидности были высокими, поскольку инвесторы и трейдеры изо всех сил пытались получить прибыль от самого продолжительного бычьего рынка в новейшей истории. Более того, люди живут дольше, и многие миллениалы начали свой инвестиционный путь с любых лишних денег в роботах-консультантах или других решениях нового века.

Но вся эта ликвидность, особенно та, которая финансировалась за счет кредитного плеча, испарится, когда начнется паника. Инвесторы без заемных средств могут покинуть позиции, но инвесторы, использующие заемные средства, будут вынужденный поскольку падение цен на 10% на рынках капитала вызывает требования маржи. Когда инициируется маржинальный вызов, капитал для его выполнения должен откуда-то поступать. Обычно это происходит в результате продажи активов, принадлежащих инвесторам, использующим заемные средства, а это означает, что цены на акции падают еще больше, вызывая дальнейшие требования о внесении маржи или, по крайней мере, усиливая понижательное давление на цены.

3 - Массовый приток пассивных средств обратится

Деньги перелились в пассив паевые инвестиционные фонды за последнее десятилетие, что заставило некоторых поверить индексные фонды приведут к следующему краху - среди них и знаменитый Майкл Берри, главный герой «Большого шорта», предсказавший крах рынка жилья перед Великой рецессией.

Подпитываемые преобладающим мнением о том, что рынок всегда растет в долгосрочной перспективе, многие люди в 2010-х годах поместили свой капитал в пассивные индексные фонды, чтобы воспользоваться этой мудростью. Однако, когда речь идет о большом количестве и масштабировании, вещи часто становятся самоподдерживающимися и даже опасными.

Приток денег в индексные фонды, особенно паевые инвестиционные фонды, означает, что эти деньги косвенно ответственны за общий рост цен. Если вы не знаете почему, см. наши образовательные ресурсы по различным типам фондов. Сейчас многие инвесторы склонны к панике, даже если мудрость дня гласит, что рынки неизбежно растут. То же самое было сказано о рынке жилья, пока этого не произошло.

Коллективная паника инвесторов означает выкуп акций паевых инвестиционных фондов, которые на сегодняшний день являются самой большой группой институциональных инвесторов. Пассивные фонды не имеют директивы по активному управлению продажами акций - как следует из их названия, они действуют пассивно - а это означает продажу акций, поскольку они отражены в портфелях фондов, для выплаты инвесторам. Это оказывает сильное понижательное давление на рынки, особенно когда долгосрочные инвесторы начинают паниковать и пытаются сохранить капитал.

4 - Денежный поток, прибыль и расходы, а также борьба за оценку

В виде потребительские расходы контракты, так же будут и денежные потоки. По мере того, как компании становятся неплатежеспособными из-за плохих денежных потоков, они больше не будут платить поставщикам, которые сами начнут бороться с денежными потоками. Ранним предупреждающим знаком был Yes Bank в Индии, который рухнул буквально на прошлой неделе.

Оценки также упадут, поскольку заоблачные оценки больше не приемлемы для испуганного рынка. Фиаско WeWork продемонстрировало, что компании сейчас сильно переоценены, но, учитывая возможность серьезного замедления роста мировой экономики, мы можем ожидать, что оценки упадут еще больше.

Даже если мы не станем свидетелями волны банкротств, мы, скорее всего, увидим падение прибыли. Индустрия туризма сильно пострадает, и на ее восстановление могут потребоваться годы, особенно если исчезнут капитал и рабочие места для тех, кто любит путешествовать. Но в широком спектре отраслей назрело снижение прибыли, в то время как падение цен приведет к значительному снижению коэффициентов ПЭ и ПЭГ. Таким образом, даже если прибыль будет падать, цены на акции, вероятно, будут падать быстрее, выравнивая отношения до более исторически нормального уровня.

5 - Центробанки остались без инструментов, но правительства все еще могут помочь

С начала Великой рецессии центральные банки использовали все имеющиеся у них уловки для стабилизации и успокоения рынков. И это сработало, но они так и не восстановили свои инструменты, чтобы сделать это снова в случае следующего кризиса.

Один из самых мощных инструментов, которыми владеют центральные банки, - это корректировка процентных ставок. Но с исторически низкими ставками дальнейшее их снижение не вариант для Европейский центральный банк, и если Федеральный резерв готов пойти в минус, у Соединенных Штатов также очень мало места для маневра.

Более того, с 2007 года экономика Китая увеличилась почти в четыре раза и теперь безвозвратно вовлечена в мировое сообщество, добавляя еще одного влиятельного игрока на мировую арену и тем самым усложняя ситуацию. Страна по-прежнему авторитарна, и Коммунистическая партия Китая (КПК) с радостью применяет жесткие меры контроля, которые могут быть весьма полезны, но могут легко напугать инвесторов, если капитал больше не может свободно проникать через границу.

Хотя денежно-кредитные инструменты ограничены, это еще не все обреченно. Некоторые фискальные инструменты все еще доступны правительствам, включая снижение налогов и спасение. Конечно, снижение налогов подразумевает меньшие налоговые поступления и обычно подразумевает сокращение государственных расходов в то время, когда расходы должны возрасти. Но правительства всегда старались уравновесить ситуацию. Спасение также может стабилизировать цены, но только после того, как они упадут намного дальше, чем 10% или около того, которое они взяли за последние пару дней, или даже когда они приблизятся к диапазону 20% за последний месяц.

6 - Потеря рабочих мест и неопределенность могут снизить потребительские и деловые расходы

Потеря рабочих мест, частично связанная с ослаблением денежных потоков и усилением контроля над расходами, может усугубить ситуацию, поскольку убытки способствуют снижению потребительских расходов и вызывают еще большие проблемы с денежными потоками. Независимо от того, теряются ли рабочие места, неуверенность и страх могут заставить многих потребителей переключиться на сбережения, а не тратить до тех пор, пока коронавирус не перестанет распространяться, что может быть проблематичным для компаний, которые уже сильно заимствованы за счет долга или едва сдерживают другие расходы.

А каналы B2B могут пострадать, поскольку каналы B2C начинают иссякать или предприятия стремятся сократить расходы, разрывая отношения с другими компаниями, пока не появится более благоприятная погода.

Стратегия ценного инвестора на будущее

Купить позже

Пришло время подождать, а не прыгать. Рынки, вероятно, продолжат падать, и мало кто умеет ловить падающие ножи. Пришло время сохранить капитал и не потерять с трудом заработанные деньги, поскольку акции продолжают снижаться. Даже если восстановление продолжается, допустимо проиграть отскок. Большинство людей не могут смириться с тем, как их положение с капиталом ухудшается из-за того, что они были обмануты краткосрочным восстановлением и попались в «ловушку быков», только чтобы позже пережить еще более резкое падение рынка.

Следите за ценностью

Конечно, в какой-то момент рыночная стоимость упадет ниже внутренней стоимости, так что ищите возможности повышения ценности с приличным запасом прочности. Будьте особенно бдительны в отношении «защищенных от вирусов» акций, поскольку они, вероятно, упадут вместе с рынками, но они могут получить «статус стоимости» задолго до других.

Короткие рынки

Сообщество стоимостных инвесторов разделяется во мнениях относительно того, является ли продажа акций «истинным инвестированием с оценкой стоимости», потому что этот подход традиционно предполагает использование длинной позиции по недооцененным акциям. Однако переоцененные акции также имеют неправильную цену, и продажа переоцененных акций в шорт аналогична покупке недооцененных акций, когда мы ищем внутреннюю стоимость. Таким образом, если вас устраивают риски коротких продаж и вы считаете, что у рынков есть значительный потенциал для движения вниз, COVID-19 и нефтяной шок могут стать триггерами, которые приведут к серьезным потерям для рынков в начале 2020-х годов.

Ищите благотворителей

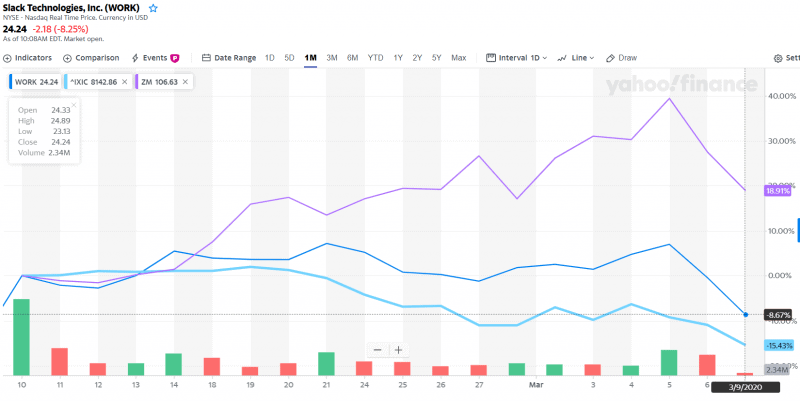

Вы также можете обратить внимание на акции «новой парадигмы», такие как Zoom или Slack, которые мы обсуждали в нашем Встречи с ценными инвесторами. Если пандемия COVID-19 продолжится, мы можем увидеть переход от стиля работы с физическим контактом к более удаленному стилю, поскольку работодателям нужны сотрудники для работы, но правительства или общества ограничивают передвижение. Slack и особенно Zoom за последний месяц превзошли NASDAQ:

Источник: Yahoo Finance.

Полезные списки наблюдения

В CityFALCON доступен наш мощный инструмент для создания списков наблюдения, которым можно легко поделиться. Ниже приведен список наблюдения, который поможет вам отслеживать COVID-19, рыночную панику и нефть. Вы можете просто щелкнуть ссылку, даже не регистрируясь, и получить последнюю финансовую информацию по этим темам.

Создайте свои собственные списки наблюдения и поделитесь ими с друзьями, коллегами или семьей или просто отправьте им ссылку ниже.

Список наблюдения за COVID-19 и ценой на нефть: http://www.cityfalcon.com/watchlists/194eeb30-a1a6-442c-94ad-d21505049255

Добавить комментарий