Lehman Brothers, AIG, Bear Stearns, Merrill Lynch, Fannie Mae, Freddie Mac, Countrywide Financial, Royal Bank of Scotland, Wachovia, Lloyds. Are these names familiar? They all suffered major upheaval or failure during the 2008 Financial Crisis, most of them being acquired by other banks or the government itself. These were all massive financial institutions, even being termed “too big to fail” – if they failed, the financial system, and consequently the national economy, would fail. Hence the bailouts, excessive quantitative easing, and emergency acquisition measures.

What ties all these banks (and one insurance company) together? The housing and derivatives market. Two behemoth markets, worth tens of trillions of dollars. The housing market not only consists of most countries’ most important assets (i.e., where their citizens take shelter), but it also represents the strength of an economy. If more people can afford to buy their own house, then the economy must be stronger – if people want to own their own house.

In this article, we will investigate whether people should buy their own home, and, if so, how they should do it. We will also look at how those decisions affect investors, and how investors can benefit (or suffer) from those decisions.

At CityFALCON, we can help keep you current on news regarding your housing market.

Government Encouragement

The government would like its citizens to pay for its own housing. Public housing projects are expensive and often concentrate poverty, which tends to exacerbate itself and leads to concentrated crime. Furthermore, people are more likely to take care of their own property than someone else’s property. Governments also make a show of helping the people.

Hence, in the US and the UK, among many other countries, there are government programs that assist home buyers. These manifest in government-backed loans and tax incentives, such as the first-time homebuyer credit in the US and Help to Buy scheme in the UK. Indeed, government-backing even incentivized banks to offer NINA loans to customers (no income, no asset). These allowed individuals to purchase housing when they could not afford it, and this buying frenzy was a major factor in the Subprime Mortgage Crisis, which eventually ignited the 2008 Financial Crisis.

New housing construction is a lucrative industry, especially when the government is willing to shovel loans into your company. Hence the drop in shares in UK homebuilders when the UK government asked the London School of Economics to evaluate its scheme – a negative outcome for the scheme would certainly mean a negative outcome for the companies.

Governments do not want their citizens homeless, and neither does society.

Social Encouragement

Owning a home is the “American / British Dream”, and this idea is prevalent in many countries throughout the world. Glossy magazines advertise breathtaking villas on remote, private beaches, and there is a pressure to be self-reliant, which means your own accommodation. Such remote locations may be cheaper than central markets like London, too, where some locales boast average home prices exceeding £400,000. Moreover, first-time buyer ages have risen, though not as much as expected.

In some parts of the UK, the average age of the first-time buyer is 27, though it can be 34 in some parts of London (Source: Halifax). The average age for the entire country is about 30. In the US, the median age hovers between 30 and 32, though this is obviously different for New York City and Billings (Montana) (Source: National Association of Realtors). Even with the rising prices and ages, there remains social pressure to buy young.

*Note the UK figure is based on an average age, and the US figure is based on median.

“Common Sense” Reasons to Purchase a Home with a Mortgage

There are plenty of reasons to buy a home, though many people internalize them as immutable fact without considering the alternatives and the factors that influence the decision. Buying a home may be right for an individual – or it may not be. The same holds true for businesses, which often can only rent spaces (i.e., in skyscrapers in the central business districts).

- Mortgage Payments are Superior to Rent Payments

First, the false equivalency of mortgage and rent payments. Some – especially realtors trying to sell homes – will claim that paying a mortgage payment is far superior to rent payments. After all, the rent payment goes directly to the landlord, while mortgage payments at least partially build your equity. In a vacuum, that is indeed true. However, this is the real world, and it is certainly not a vacuum.

The mortgage carries a massive debt with it, and this debt, while tied to the property as collateral, does not necessarily mean the equity built over time belongs to the owner. For individuals, this is especially important, because a sudden need to move can be disastrous. For businesses or investors, this is less problematic, because they need not reside in the property – you can administer a rental property from anywhere, but owner-occupied properties are fixed in place, and so are the owners.

- Housing Prices Always Rise

If housing prices rise without fail, this is actually a decent strategy. The mortgage payment will continually build equity, and eventually, the payer will own the home outright. If the owner is lucky, they might even make some money if the property price rises. In fact, many people rely on housing prices to rise, for this assumption forms the foundation of their investment.

Unfortunately, the notion that housing prices only move in one direction is absurd. The most recent crash was the subprime crisis in the United States, where housing prices plunged as entire neighborhoods defaulted. If you were an individual in the area, the economy crashed, jobs dried up, and your property was worth significantly less than the mortgage, there is an incentive to leave. However, all that money you paid in equity, plus the down payment, is forfeit.

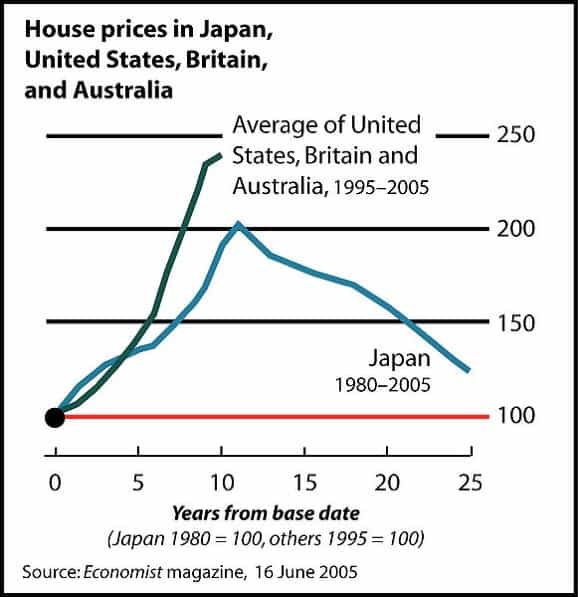

There are various historical examples of housing and real estate crashes. The Lost Decade (1990s) in Japan is partially attributed to the crash in Japanese real estate prices in the early 1990s.

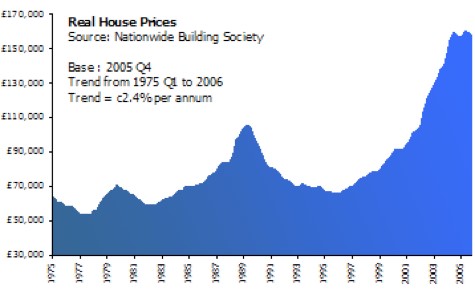

The early 1990s witnessed a property value crash in the UK, too.

Source: Wikimedia

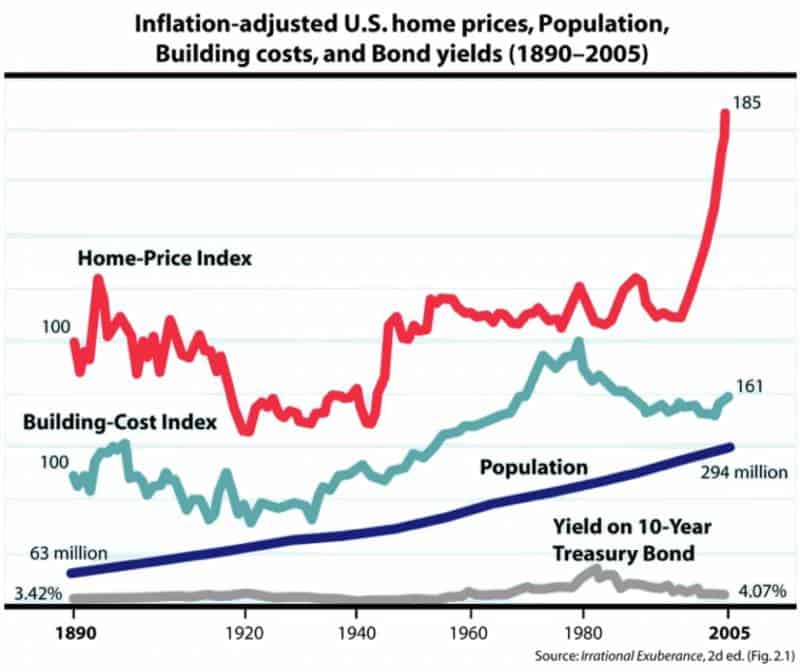

And the US suffered crashes during the Gilded Age and again after WWI, just to name a couple occurrences. As for the world in general, there have been various bubbles in the globalized world, many of which are yet to burst.

Source: Wikimedia

- The Effects of Immobility

Demographics change, people migrate, disasters happen. Since real estate is an immovable asset, it is more exposed to geographically-bound phenomena, such as migration. Furthermore, many factors influence property prices. The building of a new airport or nuclear power plant near a property tends to crush the local real estate market. Infrastructure often also invokes eminent domain, and while the process may take a while, it does eventually force property owners to sell, often at market rates. That market rate will be detrimental to the owner, as prices in surrounding areas declines to match the impact of the project

If you plan to purchase or invest in real estate, major future projects, migration patterns, and susceptibility to disaster must be primary concerns. This can mean insurance becomes a cost of buying that is absent from renting.

- Negative Equity

Mortgages are “under water” when the remaining cost of the loan is higher than the open market price of the property. For example, consider a property, purchased at $100,000 with a mortgage of $90,000 and a down payment of $10,000. After a few years of paying the mortgage (and interest payments), the mortgage principal is $75,000.

Assuming the price is the same, that $15,000 is your equity. However, what if the price of the property drops to $70,000 due to some local catastrophe? Suddenly you owe $5,000 more than what the property sells for, even though you have paid tens of thousands of dollars and years of your life into the mortgage. As an occupier, you may be incentivised to stay, but any business or investor should exit. And occupiers may not be able to remain, anyway, because the local economy has died and there is no avenue to earn income. In the worst case, the area is uninhabitable (perhaps after a local nuclear plant melts down).

This danger of under-water mortgages and property price decreases was a main reason for the Financial Crisis, and it is a good reason to carefully consider your prospects before using a mortgage, whether you will be an owner-occupier or an investor.

- Renting on AirBNB is Failsafe

In the last decade, the internet has transformed the world in many ways, One of them is the “sharing economy”, where people share their assets to generate additional income. One of the most successful vectors has been renting homes for short periods of time, and the most successful player is AirBNB.

This vector was (and still can be) a lucrative source of income for savvy investors. It allows short-term residents, who usually pay a much higher per-month rent than long-term tenants. However, because it is so much more lucrative, a housing shortage developed, with investors flooding the market to buy properties, then rent them out to short-term residents. This caused considerable consternation among long-term residents, and now many cities disallow AirBNB for that reason.

If you occupy the property, it can still be a good way to make money, but do not rely on this as a business model or a way to pay the mortgage. Laws are always changing, and such relevant laws make headlines. Investors and residents should stay aware of new regulations because it could mean the difference between money made and money lost.

Effects on the Balance Sheet and Cash Flows

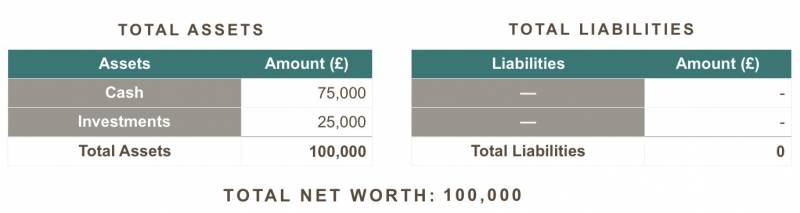

The above arguments are largely qualitatively, even if there is a quantitative counterpart. In this section, we will approach the rent-vs-buy question from a quantitative perspective. Let’s look at your personal balance sheet.

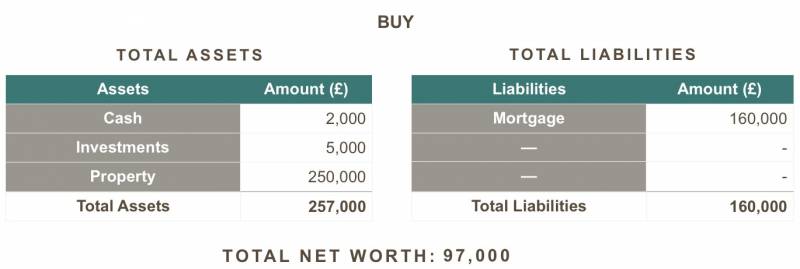

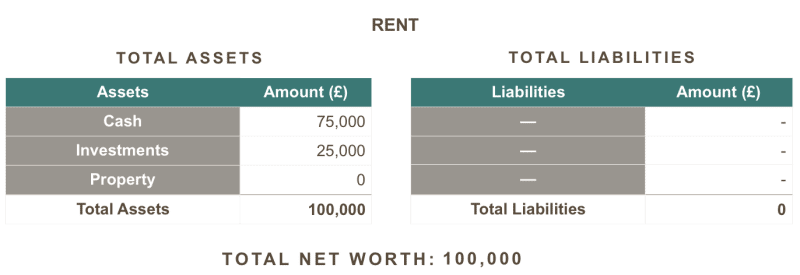

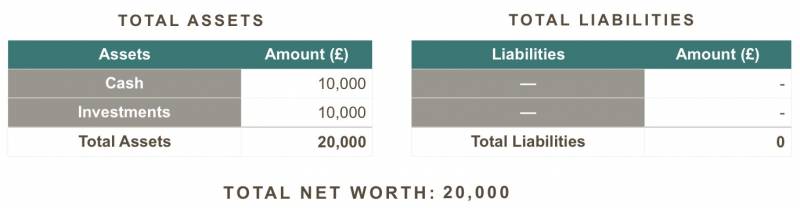

Let’s assume your only assets are liquid (i.e., cash and investments) before you decide to rent or buy. Your financial situation looks like this:

You want to buy a property worth 250,000, so you would need at least a 150,000 mortgage. Or you could rent a similar property for 850/month. Your balance sheet looks like this immediately after signing a rental or purchase agreement. The cash reserve on the buy-decision is used for survival for the first few months before liquid assets can be amassed.

Note the reduced net worth for buying. We will consider the closing costs on renting to be negligible (usually one month’s rent for the realtor’s fee plus some documentation fees).

Closing costs on a purchase, however, are usually significant. Hence a cash outflow causes a fall in equity.

How do cash flows affect the balance sheet? Indeed, the cash outflow for rent is simply a reduction in equity; for the purchased property, though, only a portion of the outflow is a reduction in equity (the interest), but the rest is added to the equity stake in the property.

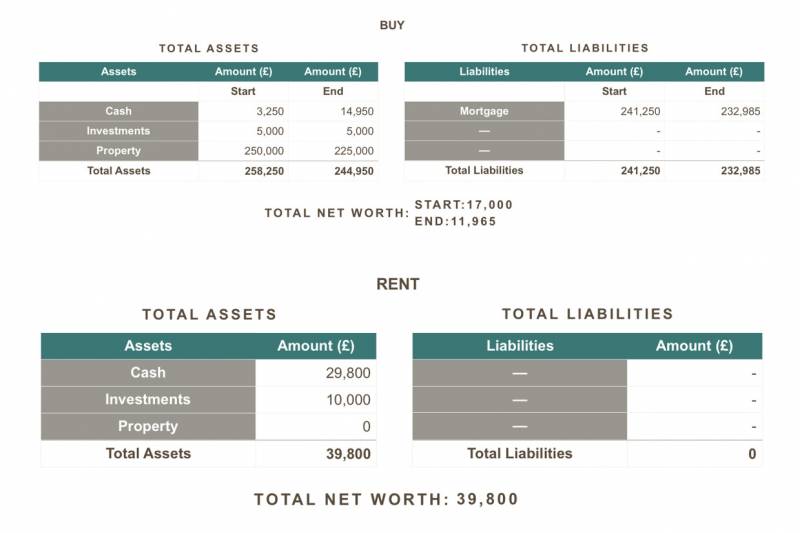

Now let’s look at those balance sheets again, but this time it will be 10 years into the future. We will assume a steady monthly income of 2,500, no property or investment appreciation, and no other payments or bills. For the mortgage, let’s use 3.5% interest rate and a 20-year term. This implies a monthly mortgage payment of 928.

From this, it seems brilliant to buy the property, because so much of your mortgage payment is retained in equity in the property. However, what if you lost your job and needed to move within one year? Furthermore, let’s assume you lose your job because the housing market crashed and the local economy suffered, so your property’s value has fallen 10%.

Since the owner must vacate and sell the property, which is now only worth 225,000 on the market, the final equity is much lower. Additionally, this is only a 10% decrease, and the mortgage is certainly not “under water”. During the height of the Subprime Crisis, the S&P Case-Shiller Index, which tracks prices in 20 US cities, fell by 18% over one year. In some cities, prices were down over 30%!

To show how price declines and high leverage can result in underwater mortgages and negative equity, let’s look at an example in which the buyer is highly levered – and hence more exposed to risk. Let’s assume a 10% decrease. Our assets are much lower, which means a lower down payment (3.5%), a higher interest rate (4.5%), and a higher monthly payment (1,525). Investors with high capital may view this as a lower down-payment and high leverage investment on a rental property.

This scenario is again after one year, and we combined the start and ending positions into one table for the buy decision.

Here, the owner’s equity for the property is negative, which means the loan owed to the bank is greater than the property value. Moreover, this example assumes there are no other payments at all, but owners who also occupy their houses have bills. Not only does this scenario only leave 975 for the bills, food, and other necessities, that is a very low estimate for monthly costs of home ownership. When assuming any amount over 975 for other expenses, the cash balance actually falls, and this is how people end up with no assets and loan principals greater than their collateral, i.e., negative overall equity.

The rental scenario leaves 1,650 for bills, and there is no need to pay homeowner’s insurance, maintenance, and even some utilities (heating, water, and sometimes electricity are sometimes included in rent). Crucially, if the price of the property falls, the renter loses no equity, because they derive no equity from the property.

A Few Things to Consider

Before renting, there are many things to consider. Here are a few important points, but they are by no means exhaustive.

- Reduce Leverage as Much as Possible

It may be tempting to take out a large mortgage and keep a lot of liquid assets, but this only serves to dramatically increase your interest rate and exposure to risk. Considering the above calculations, if the property’s value falls, the difference comes out of your equity: you still owe the bank whatever mortgage principal remains. The greater your mortgage-to-equity ratio (i.e., the greater your leverage), the more risk you carry.

- Costs of Buying (and Selling) a Property

The one-time and recurrent expenses of renting are relatively low. There is generally a realtor fee, perhaps some documentation fees, and furnishing purchases. The recurrent expenses are even lower because maintenance and grounds upkeep are often paid through rent.

The costs of buying a house, though, can be significant. The one-time costs, such as realtor fee, origination fees (for the mortgage), furnishing purchases, and building inspections can rapidly increase. A couple percentage points here and there may seem insignificant, but a large amount of capital involved ensures these costs quickly become a significant amount. Moreover, renovations, whether required or voluntary, can comprise a significant portion of costs.

When owning a home, the recurrent costs, such as maintenance and upkeep, are solely the responsibility of the property owner and no one else. Certain bills are associated with home ownership, such as home insurance, that is often not applicable to rentals.

At the other end of the time period, when the owner decides to leave the property, selling costs include appraisals, realtor fees, and even mortgage penalties if the mortgage carries a “prepayment penalty” clause. For rentals, there may be a lease termination penalty, but in general, renters can simply vacate the property after a year without penalty or before a year with sufficient notice. A one-year lease is much shorter than a 30-year mortgage.

- For Investors, REITs and ETFs may still give the upside

If your main goal for purchasing a property is appreciation or rental payments, REITs are an option. These expose the investor to the real estate market and may securitize cash flows or reflect property value appreciation. Since REIT investors have no legal obligation to banks or property owners, they do not incur any liability and their investment cannot result in negative equity (unless, of course, you’re shorting or levered).

As with almost any financial concept, there are also ETFs that invest in real estate companies instead of directly into a property. This is another avenue to gain exposure to real estate, though this focuses more on the residual income from property exchange (i.e., whatever the real estate company makes in buying or selling) rather than income generated by the properties.

The Debate Goes On

It is less a debate about which is better as a whole, and more a calculation for each individual or business to evaluate. Buying property is not inherently detrimental to financial health, and in fact, it can be quite beneficial. However, speculation can be risky, especially on price movements for such large, illiquid, and immovable assets. For those who plan to remain at the property for a long time, the benefits of buying can easily outweigh the detriments. Those who can purchase property in full and in cash are also at an advantage because there is no risk of negative equity.

For most people and small businesses, however, it is simply infeasible to purchase a property in cash without incurring some debt. For such property-seekers, it is highly advisable to consider all the points outlined here and to do further research, specifically regarding their chosen markets.

Unfortunately, there will be no bailout for individuals or small businesses. Hence, they must understand the balance sheet and cash flow impacts of movements in the market, changes in the relevant regulations, and variations in social, political, and economic trends.

14/09/2017 at 12:02 pm

Thank you for the tips! I always thought about having a good leverage is a must. Good to know!