Disclaimer: This is a guest post from Michael, and does not reflect the views of CityFALCON and its stakeholders.

Stock: Gulfmark Offshore (NYSE:GLF)

Date: 1/11/2016

Current Market Price: $1.10

Price target over two years: $5 per share, possibly $10-$15

Downside risks: This is a micro-cap stock with only $28m in market capitalisation, and can be very volatile on a daily basis. Please consider the risks and talk to a financial advisor before investing.

Background:

GLF provides marine support and transportation services to companies involved in the offshore exploration and production of oil and natural gas.

GLF’s vessels transport drilling materials and personnel to offshore facilities, and also moves and positions drilling structures. GLF’s vessels service the offshore exploration and production sectors of the oil and natural gas industry. Everyone knows that we are going through an energy slump, my thesis is that we appear to have hit the bottom and oil and gas are starting to rebound.

From Wall Street Journal:

“In his five months as Saudi energy minister, Mr. Falih has overseen a significant change in the kingdom’s oil policy, turning it away from strategies aimed primarily at surviving an era of ultralow prices. Mr. Falih has instead pointed the kingdom back in the direction of its traditional role of stabilising prices by regulating the output of OPEC, the 14 nation cartel that controls over a third of world crude production Mr. Falih said, citing an increasing car fleet in China and rising consumption in India.”

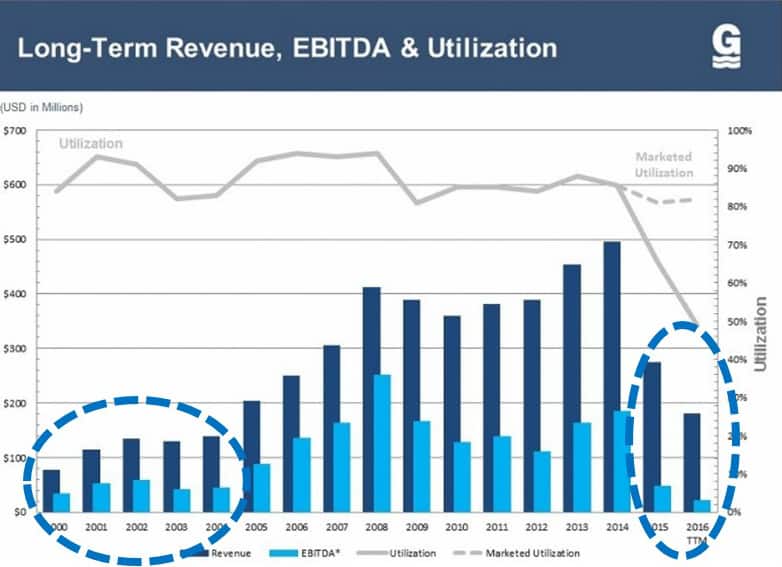

If you compare the price investors were willing to pay for GLF in 2000-2004, say $13, with what investors are willing to pay for now, you should agree with me, that today at ~$1.35 it is cheaper? In the graph below, compare the Revenue and EBITDA of 2004-2004, with now. Presently, GLF has significantly higher revenues, greater market position and strength, in spite of the downturn. This company is clearly selling vessels that oil companies need. EBITDA levels are a little lower, but not enough to warrant the sell-off down to the price of $1.35.

We are at a trough in the oil market, no doubt. But the question is, has the bottom been found?

Source: GLF’s presentation, August 2016

Financials:

The financials are interesting. The bad news is that, out of all of the earnings that the company has generated, they only kicked out a few years of dividends.

But the really good news is that they have invested a lot of capital into their vessels, and this is all accounted for on their balance sheet, giving us downside protection. Sure, the vessels are not worth the $1B on their balance sheet. But GLF has been impairing the value of its vessels since last quart of 2014 (more on this below). Another really good bit of news is that this company’s vessels clearly have a market. This is demonstrated by the fact that up to full year 2015, they had been growing revenue, going from $251m all the way up to ~$500m or 100% growth over the 9 year period. There is clearly demand for GLF.

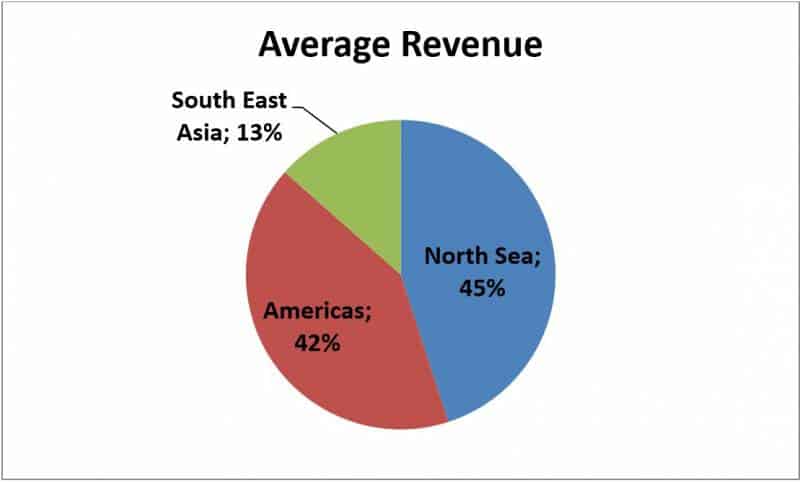

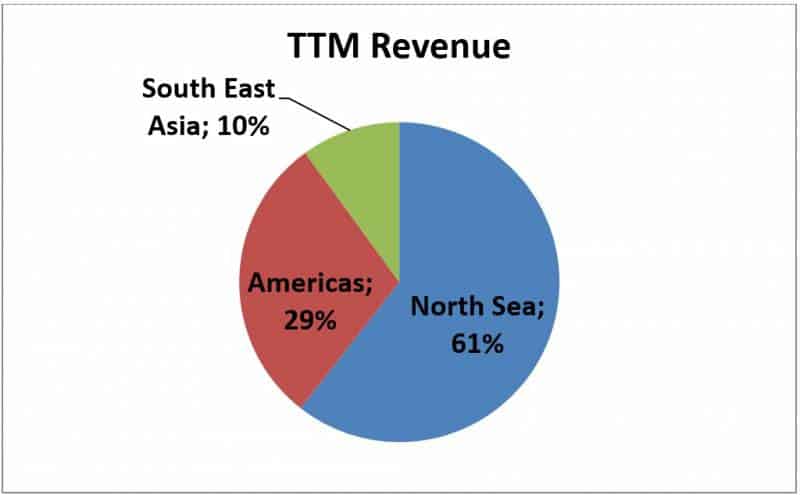

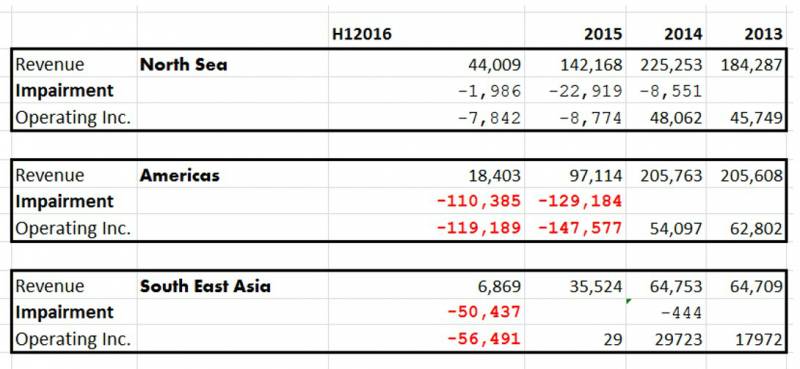

GLF’s Operating Segments:

Source: Author calculations.

Although GLF has 3 operating segments, from a revenue perspective we should be interested in 2, North Sea and Americas. These two are its bread and butter. However, in the trailing twelve months, the Americas segment has fallen dramatically. (See below, table & graph):

Source: Author calculations.

Source: Author calculations.

As you will notice in the table above, the North Sea segment has remained strong at ~$44m. And on superficial analysis, a lot of investors will have shun away from GLF. But if we look a little deeper, we can see that the non-cash impairments came from Americas and its tiny South East Asia operating segment. So, the market has massively over-reacted on this one, and the selloff is not warranted.

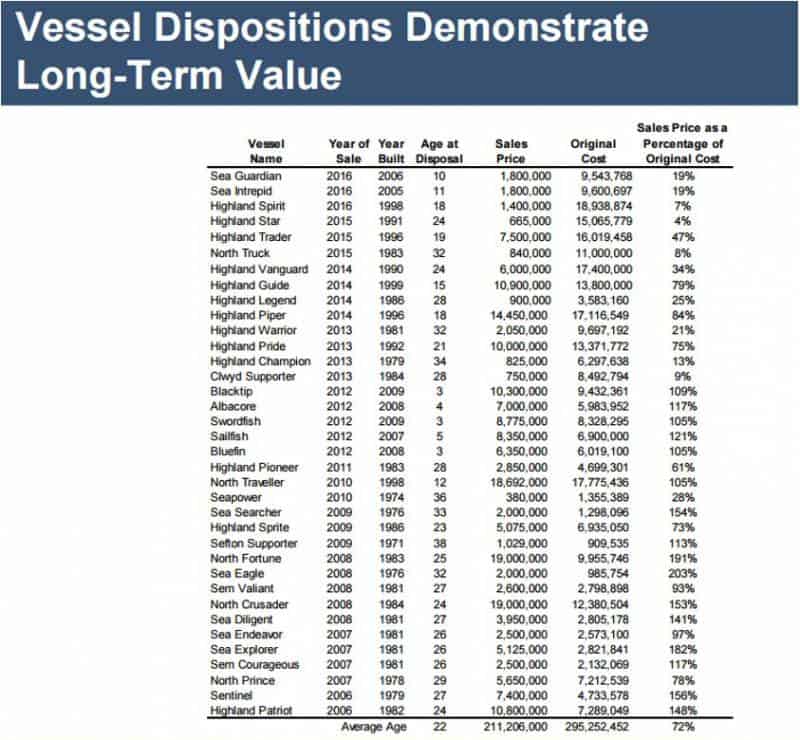

Vessels:

“ A large factor in the impairment process is the assets’ appraised value (we receive quarterly third party appraisals) which one could assume approximates its fair value.”

– Personal correspondence with GLF’s investor relation

“The vast majority of [Long-lived assets on the balance sheet, is made up of] vessels , equipment, and other fixed assets is made up of our vessels. Probably more than 95% are the vessels. There rest of the value is other equipment, spares, etc.”

– Personal correspondence with GLF’s investor relation

At current prices, our downside is being protected by the assets on the balance sheet. The assets have been impaired every quarter since last quarter of 2014. An independent firm was hired to value the vessels and off that, the impairments have been based on. After so many impairments, it is fair to say, what you see is what you get. Even if do our own discounting further on the fixed assets on the balance sheet, we still have plenty of margin of safety on this stock purchase. I have been in touch with the GLF’s investor relation (excerpts above) and while they would not offer me any specific numbers they did confirm that the assets are close to fair value, in spite of the impairments and low vessel valuation.

Source: GLF presentation, August 2016

As you will notice in the table above, the sale of vessels during the downturn since 2014, are still being sold for something. Although, of course, heavily discounted.

Impairments:

So, here is the thing, by now, you understand that we are going through a grim and long downturn in the energy market, specific to GLF, being the oil and gas downturn. But the thing that is actually causing GLF’s financials to look so grim are only partially revolved around their core sales. Carefully look at the table below focusing in on the red font.

Source: Author calculations.

“[…] recorded $114.1 million of impairment charges in the first quarter of 2016 and $46.2 million in the second quarter of 2016. The first quarter impairment consisted of $94.5 million in connection with our long-lived assets in the U.S. Gulf of Mexico, which is part of our Americas segment […], and $19.6 million in connection with our Southeast Asia segment. […] impairment consisted of $15.9 million in the Americas asset group that is outside the U.S. Gulf of Mexico and an additional $30.3 million in our Southeast Asia segment”

– 10K 2016

So while the non-cash impairments have been killing the financials, once we dig deeper, things aren’t so bad. GLF does not give up a lot of detail into the location of their long-lived assets apart from in their country of domicile, the US, but they do disclose that in US alone they have ~$366m in tangible capital. I think that at ~$40m Market Cap, we are quite well compensated for the worst.

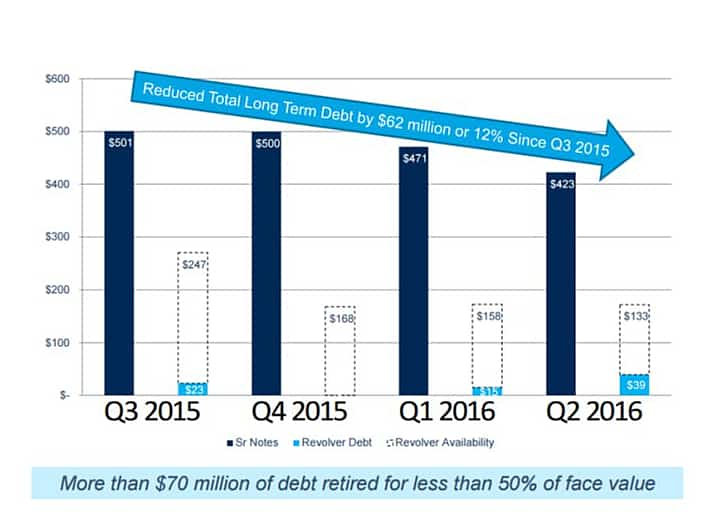

Financial position:

The debt situation is a mess. It is really ugly. But the Revolving Credit Facilities were Renegotiated in January 2016 and now mature in 2019. The secured debt (~$420) matures in 2022. At June 30, 2016, cash on hand was ~$11 million, ~$39 million drawn on revolver, available borrowing capacity ~$134 million; Total liquidity ~$145 million.

Source: GLF presentation, August 2016

Source: http://finra-markets.morningstar.com; GMRK3956992

Generally speaking, institutions that invest in bonds are very risk averse. Much more risk averse than equity traders. GLF’s secure debt, has recovered considerably from the trough of January 2016. But GLF’s equity continues to selloff. Investors are disgusted to own GLF. This allows Value Investors, that are emotionally detached and focused on fundamentals to pick up GLF cheaply.

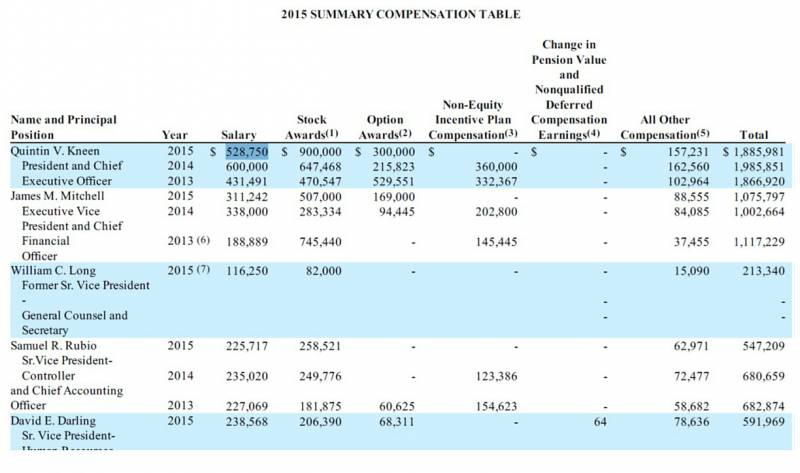

Insider Ownership

Insiders are not been paying silly salaries and by far, the vast majority of the remuneration is tied up to GLF’s stock price. Also, all the stock options are out of the money (strike price ~$13). So if the share price does not increase, they don’t get much money, so it is in their interest to move up the share price.

“Base salaries for our executive officers were reduced by 15% for our Chief Executive Officer, by 10% for each of our Executive Vice Presidents and by 5% for our Senior Vice Presidents”

“In light of industry conditions, negative discretion was applied and no cash bonus was paid in 2016 for the 2015 performance year to any of our employees, including executive officers”

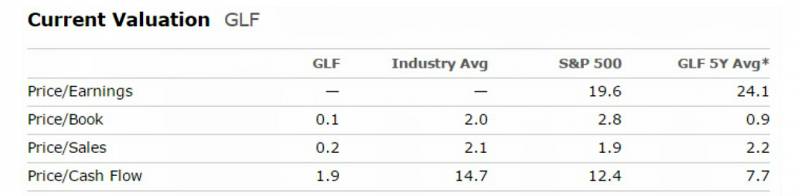

Comparing GLF’s valuation with competitors:

GLF:

I like to compare the P/S on the 5 year average with the current P/S. Investors were willing to pay about ~2.2x Sales, or ~$800m-$900m Market Cap for GLF over the last 5 years, now it trades for only ~$40m.

Tidewater Inc. (selling for roughly same valuation as GLF; but with huge liquidity issues). As we write, it is facing Chapter 11.

Halliburton Company (overvalued; which is near enough insane, during the oil downturn.)

SEACOR Holdings Inc (close to fair value). Interestingly, being a significant bondholder of GLF’s debt, it has made a small tentative call for acquisition of GLF. Although, not seriously being considered by either company, it shows that there is huge value in GLF business, so much so, that its main competitor is willing to acquire GLF’s debt of ~$460m!

Possible catalyst:

Here are two graphs to help me what I want to say (below). We are clearly off the bottom of the cycle. But this has not reflected itself in some of the smaller cap companies. A lot of these companies, are cheap for a reason. Value Investor’s job is to find the handful that we think the market has got wrong, and from that small group, pick the safest stock.

Source: Nasdaq.com

Conclusion:

I’m not into timing tops and bottom of commodity cycles, but I suspect that possibly the worst is over. Again, the recovery will be very long, but it will come. In the words of the Saudi energy minister Mr. Falih “an increasing car fleet in China and rising consumption in India […] will lead the recovering”. I don’t know when, but at the current price we are being compensated to wait and see.

If you’d like to track real-time relevant financial news for Gulfmark Offshore (NYSE:GLF), check it out here.

Leave a Reply